Team Arro

Table of Content

Why APRs Are Increasing

Why Credit Card Interest Rates Matter

How Do Credit Card Interest Rates Affect My Monthly Statement?

How Arro Is Different

Take Control Of Your Credit Journey With Arro

FAQs

Opening up a credit card statement these days can feel like bracing for bad news. In 2022, credit card interest rates, or Annual Percentage Rates (APRs), have already climbed substantially since the Federal Reserve began raising the prime rate, affecting both existing cardholders and anyone shopping for new credit cards.

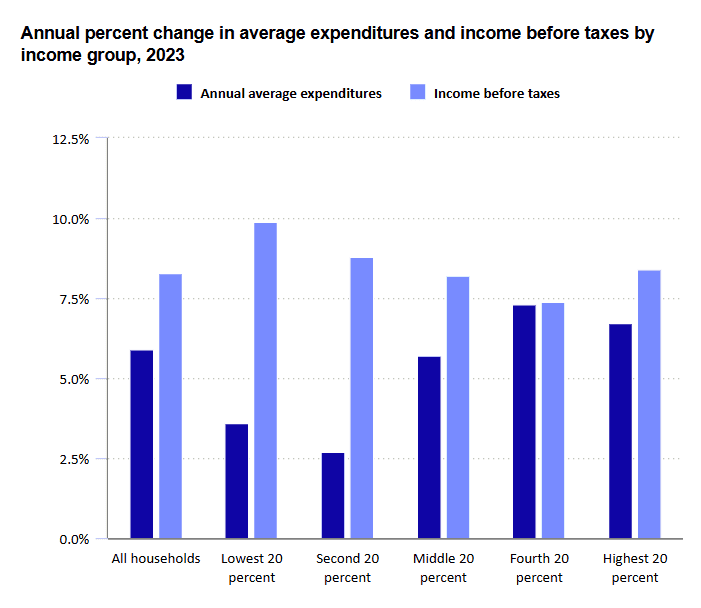

According to the U.S. Bureau of Labor Statistics, consumer spending increased 5.9 percent from 2022 to 2023, yet many households are seeing their interest charges eat into their spending.

Source: U.S. Bureau of Labor Statistics

In this article, we'll break down why APRs are increasing, what does fed rate hike means for your monthly payments, and the ways the Fed interest rate could impact your finances both now and in the future.

Key Takeaways

Federal rate hikes automatically trigger increases in credit card APRs on most variable-rate cards.

Banks aren't required to notify you when APRs rise due to Fed changes.

Understanding interest rates and tracking their changes can help you anticipate higher monthly costs on carried balances.

Even small increases in APR can add hundreds of dollars in annual interest charges on carried balances.

Arro keeps rates nearly 50% lower than competitors while helping you build credit responsibly.

Why APRs Are Increasing

When the Federal Reserve raises interest rates, this increases the price that banks have to pay to borrow money from other banks, called the Federal Funds Rate. This makes it more expensive for banks to raise funds to lend, whether by borrowing from different banks or by offering higher yields on deposits. Just like an increase in the price of aluminum might make cars more expensive to produce, a rise in interest rates makes lending more expensive.

When this occurs, banks can either keep the price unchanged, reducing their profit margins, or pass the price increase to consumers through higher APRs. Most credit cards have variable interest rates. This means the interest rates you see on your statement are tied directly to a specific index and change whenever it changes. As the Fed raises interest rates, your credit card APR will increase automatically.

Understanding “What does Fed rate hike mean?” is crucial for managing your finances. When the Federal Reserve increases rates, it ripples through the entire economy, affecting everything from mortgage rates to credit card APRs. The ways the federal interest rate could impact your finances include higher borrowing costs and better returns on savings accounts.

Shouldn't My Bank Notify Me When They Increase My APR?

The bank doesn't need to tell you if your APR increases for this reason, so if you were wondering why the interest rates you see on your statement seem higher than they did a few months ago, this is likely the answer. The good news about variable interest rates is that the rates will automatically decrease again when the same index falls, so if the Fed lowers rates, the rates on your existing cards will decrease as well.

So, Should I Open A New Credit Card With A Lower Interest Rate?

The Federal Funds Rate also determines APRs for new credit cards, but the relationship is more indirect. Since these APRs only affect new customers, credit card companies don't need to comply with a Cardholder Agreement that promises to reduce rates when the Funds Rate declines, just as they increased them when it rose. This means that when you see interest rates on new card offers, they often remain high even as the Prime Rate decreased during the pandemic.

When shopping for new cards, you'll notice interest rates from competing issuers cluster within a similar range, reflecting the current Federal Funds Rate environment. The challenge is finding a card that offers rates significantly below the market average while still providing value.

Why Credit Card Interest Rates Matter

APRs are difficult to understand, making it challenging to make fully informed decisions about which credit cards to get and how much to use. In short, APRs are the price you pay for holding credit card debt. This means higher interest rates will cause debt to accumulate faster if you aren't paying your full balance each month.

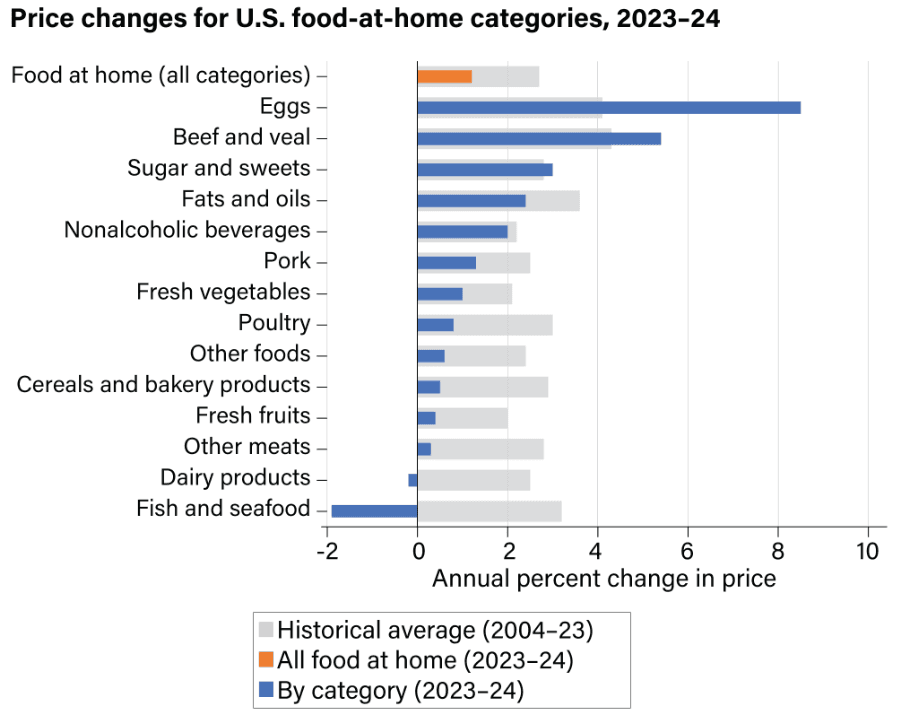

Understanding how the federal funds rate could affect your finances helps you make smarter decisions about carrying balances. According to the U.S. Department of Agriculture's Economic Research Service, U.S. consumers spent $2.58 trillion on food and beverages in 2024, with food-at-home prices increasing 1.2 percent. Every dollar spent on interest is one less dollar available for essentials like groceries.

Source: U.S. Department Of Agriculture

Furthermore, interest charges often go directly into your minimum payment calculation, so all interest that you accrue this month will be part of the minimum payment you are required to pay next month. This creates a cycle where:

When you see that interest rates have increased, larger interest charges follow

Larger interest charges increase your minimum payment

Higher minimum payments strain your monthly budget

These interconnected factors make understanding and managing your APR essential for financial health.

How Do Credit Card Interest Rates Affect My Monthly Statement?

In early 2022, you would be charged $117 per month in interest on this balance at a 27% APR. At a 30% APR, you would be charged $130 per month in interest. This adds up to more than an additional $150 in credit card interest you are paying every year - money that isn't going to bring your debt down, but just to stop it from getting larger.

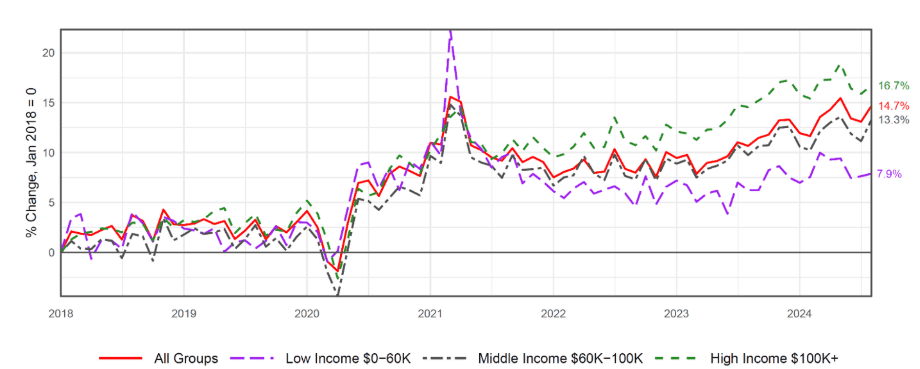

Source: Federal Reserve Bank of St. Louis

To put this in perspective, the Federal Reserve Bank of St. Louis reports that as of August 2024, real average spending by low-income households is up only 7.9% relative to January 2018, while middle-income households' spending increased 13.3%. That extra $150 in annual interest charges represents a meaningful portion of limited household budgets.

How Arro Is Different

You're probably wondering one of two things:

Arro will definitely save me some money, but that's still a lot of interest!

How can you afford to charge so much less than your competitors?

To point number 1, we completely agree! This is why a low interest rate is only part of what Arro offers. Arro was built using a behavioral science-backed approach to help you build credit while staying out of debt. Our model is built around making large payments, so that in most months, you pay no interest on your debt. That will keep your credit score high and your interest payments low, while giving you credit at the lowest interest rate we can provide you in case of emergencies.

Understanding what a fed rate hike means and how it affects traditional cards helps highlight Arro's advantage: while other issuers immediately pass along rate increases to maximize profits, Arro keeps rates stable to support your credit-building journey.

Also read:

Credit Cards 101: Here’s What Happens if You Go Over Your Credit Limit

It’s All About the Plastic: Charge Card vs. Debit Card vs. Credit Card

Balance Transfer Or Personal Loan: What Is The Right Fit For You?

Take Control Of Your Credit Journey With Arro

Understanding how Federal Reserve decisions affect interest rates is the first step toward taking control of your financial future. While most credit card companies see rising rates as an opportunity to increase profits, Arro takes a different approach. We believe building credit shouldn't be expensive or confusing.

That's why we've created a credit card that supports you in learning, earning, and growing, all in one app. With no hard credit checks, no deposit, and 1% cashback on gas and groceries, Arro makes it simple to start improving your credit while rewarding your everyday spending. You'll also get access to Artie, your personal AI Money Coach, who's there 24/7 to answer questions, celebrate wins, and help you make smart financial moves.

Every on-time payment, every lesson, every small step forward helps you unlock higher credit limits and better credit health. Thousands of people are already building stronger credit with Arro and enjoying the journey.

See how easy it can be to build credit with confidence – no matter what the Fed decides to do with interest rates.

FAQs

How quickly do credit card companies adjust APRs after a Fed rate change?

Most issuers adjust variable APRs within one to two billing cycles after a Fed announcement. Some apply changes immediately, while others wait until your next statement closes. These changes happen automatically without notification, so when you see interest rates have increased on your statement, the change likely occurred weeks earlier.

Can I negotiate a lower APR with my credit card company even after the Fed rate increases?

Yes, you can always try negotiating. Success depends on your payment history, credit score, and customer tenure. Before calling, review competitor card interest rates so you can mention better offers during your negotiation.

What's the difference between a fixed APR and a variable APR in today's rate environment?

Variable APRs are tied to indexes like the Prime Rate and adjust automatically without notice. Fixed APRs stay stable unless your issuer changes them with 45 days' advance notice. Since 2022, variable rates have increased multiple times automatically, while fixed rates have changed only when issuers raised them explicitly. When you see interest rates on new card offers, knowing whether they're fixed or variable helps you predict future costs.

Does carrying a balance on multiple credit cards amplify the impact of Fed rate increases?

Yes, significantly. If you have three cards with $2,000 balances each, and each increases by 3%, you're paying extra interest on $6,000 in total. Each card calculates interest independently, making it harder to pay down principal. Consider consolidating into a single lower-rate card or tackling the highest-rate balance first.

How can I protect myself from future Federal Reserve rate increases that could affect my finances?

Pay off balances completely each month to eliminate interest charges. If that's not possible, consider 0% balance transfer offers or build an emergency fund to reduce reliance on credit cards. Improving your credit score can qualify you for lower interest rates on cards. Starting with products like Arro, which offer substantially lower APRs, provides built-in protection.