Arro Team

Table of Content

What Is An 800 Credit Score?

Benefits Of An 800 Credit Score

Tips For Working Toward An 800 Credit Score

Build Your Credit Journey With Arro

FAQs

Reaching an 800 credit score offers so many benefits. When you have excellent credit, lenders are more likely to approve your application for a mortgage, auto loan, or personal loan.

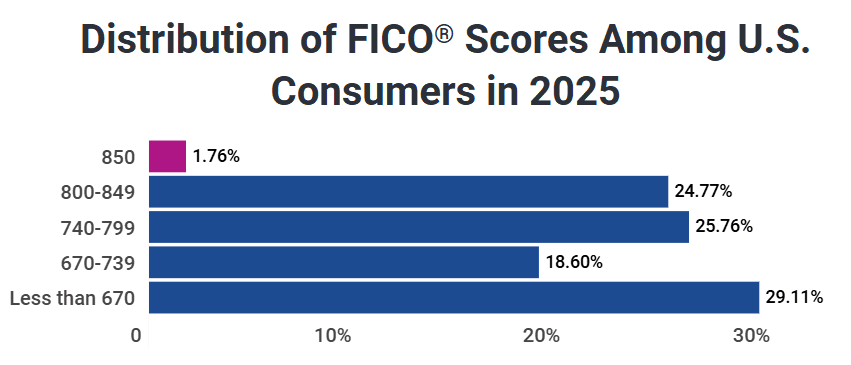

Lower interest rates and higher credit limits are also among the perks. According to recent data from Experian, only 24% of Americans have FICO scores between 800 and 850, which is regarded as exceptional credit. Even more impressive, just 1.76% of consumers have achieved a perfect 850 credit score as of March 2025.

Source: Experian

In this article, we'll explore the benefits of an 800 credit score, what it takes to achieve it, and how you can start working toward this important financial milestone.

Key Takeaways

An 800 credit score places you in the top 24% of consumers, qualifying you for the best rates and terms.

Payment history makes up 35% of your FICO score, making on-time payments the most critical factor.

Reaching an 800 credit score typically requires at least 15 years of consistent credit history.

Keep credit utilization below 30%, or ideally below 10%, to maximize your score potential.

An 800 score opens doors beyond borrowing, affecting job prospects, rentals, and insurance rates.

Monitor your credit reports regularly, as errors are common and can harm your score.

You don't need to be debt-free; strategic debt management with a mix of credit types is more beneficial.

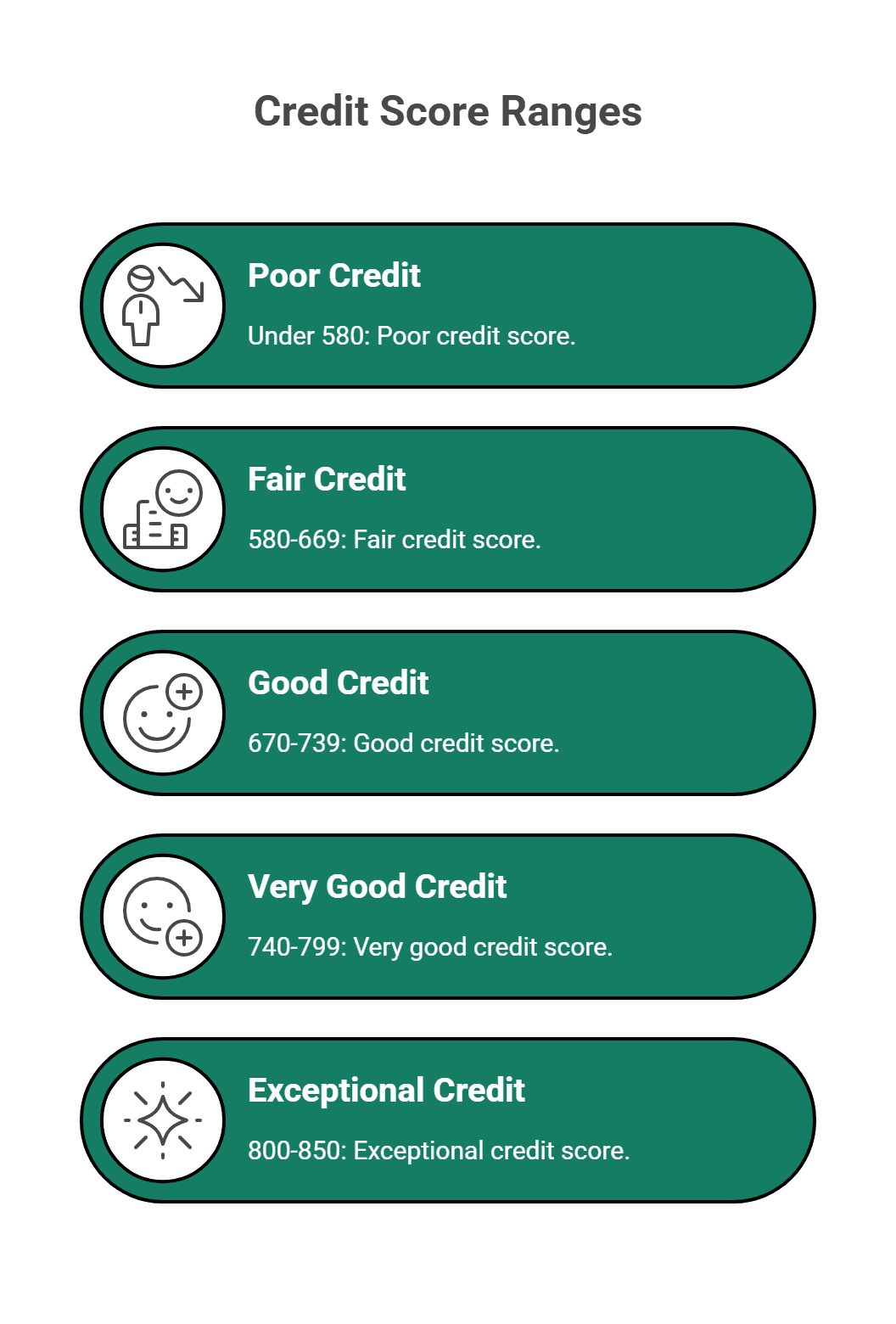

What Is An 800 Credit Score?

When making credit decisions, lenders rely on a borrower's FICO score, a measure of their credit management over time.

The FICO scoring system ranges from 300 to 850. Here's what this credit score range means:

Keep in mind that about 35% of your FICO score is based on your payment history. It's important to pay your bills on time to improve or maintain your FICO score.

It's also important to know what FICO doesn't take into account. The following doesn't affect your FICO score:

Age

Gender

Race

Marital status

Education

ZIP code

These factors help create a fair assessment of your creditworthiness based solely on how you manage debt.

Is 800 A Good Credit Score?

Yes, absolutely. It's exceptional. Financial professionals have noted that credit scores in the high 700s are usually sufficient for applicants to get the best loans and top-tier credit cards. Some see 760 as a key threshold for the best mortgages, and even a slightly lower score for the best car loans. An 800 credit score puts you well above these thresholds and into elite territory where you'll receive the most favorable terms available.

Benefits Of An 800 Credit Score

When you have an exceptional credit score, the world is your oyster, credit-wise. You can typically qualify for almost any line of credit at a better rate. Credit card issuers offer you their best rates and all sorts of perks (and higher credit limits, whether you need them or not). Here are the financial advantages you get:

Lower Interest Rates Across All Loans

You're also likely to benefit from lower car loan and home insurance rates. Or maybe you took out a mortgage with a higher interest rate when your credit score was lower. Once you reach an 800 credit score (or even close to it), you can think about refinancing. Your higher score will help you secure a better rate, potentially saving hundreds of dollars on your monthly payment.

Premium Credit Card Offers

An 800 credit score means you're the type of customer that credit card issuers want, which translates into receiving the best credit card offers. Think: zero-percent promotional rates on purchases and balance transfers, or generous, ongoing rewards bonuses. For instance, you could get high cash-back percentages from certain retailers, restaurants, travel purchases, and more. Of course, just because you have access to these perks doesn't mean you have to use them, especially if it means spending money unnecessarily.

Better Job And Housing Opportunities

An exceptional credit score can also relate to job and housing opportunities. Employers and landlords often run credit checks, so an 800 score can mean the difference between landing a job or an apartment and not. If you're competing for a job, someone with a stronger credit history might be perceived as more responsible and hired ahead of you. When securing an apartment lease, those with lower credit scores may be required to pay a higher security deposit.

One of the greatest benefits of an 800 credit score is psychological. Possessing excellent credit gives you more options in life. And who couldn't use some extra peace of mind?

Tips For Working Toward An 800 Credit Score

The key to achieving an 800 credit score is financial discipline. This might not sound like fun, and reaching the 800 level doesn't happen overnight, but it's possible if you stay focused over the long term. Let's break down some strategies for how to get 800 credit score:

Use Your Credit Card Regularly And Responsibly

While you should use your credit card regularly, be sure to pay your bill in full each month so you don't carry a balance. As a bonus, you won't pay interest on your purchases. And of course, avoid late payments or missed payments, which immediately decrease your credit score.

Have A Good Credit Mix

FICO prefers a mix of credit types. Besides credit cards, that might mean a mortgage, auto loan, personal loan, or student loan, all of which are installment loans. You borrow a specific amount of money and pay it back over time, with interest. Once it's paid off, the loan closes.

Credit cards are considered revolving credit, meaning you can pay the entire balance off in full at once or in smaller amounts over time, with interest. The line of credit remains open as long as you pay the minimum balance.

Keep Your Debt-To-Credit Ratio Low

Your credit utilization rate is the same as your debt-to-credit ratio. Determine your credit utilization ratio by dividing your available credit by your total debt on those credit accounts. This only includes your revolving credit lines (e.g., credit cards), not installment loans (such as a car loan).

Keep your debt-to-credit ratio at 30% or less for now. That means if your available credit is $10,000, your debts should remain at about $3,000 or below.

As your credit score rises, try to reduce your credit utilization to 10%. In other words, keep your credit card balances low. We know it's tempting to book a spring break vacation and put it on your credit card. But if you don't have the funds to pay it off right away, it'll put you further from your financial goals in the long run.

Having credit cards without other types of credit can lower your credit score. A personal loan can boost your credit mix, but only apply for new credit when you need it. For example, if you're carrying a credit card balance, a lower-interest personal loan lets you pay it off while improving your credit mix.

Keep An Eye On Your Credit Reports

What exactly will you be looking at when you check your credit report? Here's what it includes:

Credit accounts

Credit inquiries

Collections (unpaid debt that goes to a collection agency)

Public information, such as bankruptcy

Personal information, including current and past addresses, phone numbers, birth date, and Social Security number

Any errors can really harm your score or be a sign of identity theft (yikes!), which is why you should check it regularly. If you see any credit activity or accounts you don't recognize, let the credit reporting agency know right away. You can take advantage of AnnualCreditReport.com to keep an eye on things, which offers a free credit report annually from each of the three major credit bureaus.

For a fee, you can also subscribe to a credit monitoring service. The service will send you an alert immediately if it flags suspicious activity. Some credit cards and banks even offer free credit monitoring as a perk.

Also read:

Build Your Credit Journey With Arro

Achieving an 800 credit score is a journey that requires patience, discipline, and the right tools to support your financial growth. While reaching exceptional credit takes time, having a partner that makes the process easier and more rewarding can make all the difference.

At Arro, we believe building credit shouldn't be confusing, expensive, or out of reach. That's why we've crafted a credit card that supports you in learning, earning, and developing, all seamlessly integrated within a single app. With no hard credit checks, no deposit, and 1% cash back on gas & groceries, Arro makes it simple to start improving your credit while rewarding your everyday spending.

You'll also get access to Artie, your personal AI Money Coach, who's there 24/7 to answer questions, celebrate wins, and help you make smart financial moves. Every on-time payment, every lesson, every small step forward helps you unlock higher credit limits and better credit health.

Thousands of Arro members are already building stronger credit and enjoying the process. Ready to start your own journey? See how easy it can be to build credit with confidence. All you need is your bank account and Social Security number to check whether you qualify for an Arro Card.

FAQs

Is An 800 Credit Score Rare?

While not super rare, an 800 credit score is considered an exceptional credit score. The highest credit score isn't far off, at 850. According to recent data, the average credit score is 717, which is considered a good credit score.

How Many People Have A Credit Score Over 800?

Just 24% of consumers have FICO credit scores of 800 or above. Want to be one of them? Follow the strategies we've shared, and you'll be on your way to getting the best rates and perks when it comes to financial services.

How Many Years Does It Take To Get An 800 Credit Score?

We're not going to lie, it can take many years to achieve an 800 credit score. To reach an 800 credit score, the length of your credit history is usually a minimum of 15 years. Lenders need that timeline to see you've established good credit habits. Even if you have bad credit now, don't despair. It's certainly possible to improve your credit score over time and achieve a good score. It takes patience, diligence, and responsible credit management, but it's not out of reach. The best day to start is yesterday; the second-best is today.

How Much Can I Borrow With An 800 Credit Score?

It depends on several factors, such as your annual income, employment status, how long you've been at your job, and how long you've lived at your current address. Every person's situation is unique, but generally, a higher credit score can help you access larger credit limits at more favorable rates.

Can I Buy A House With An 800 Credit Score?

Yes! An 800 credit score is generally considered good if you're in the market to purchase a home. You should qualify for the best interest rates. However, you'll still need money for the down payment. One note: If you're buying a house with a spouse who has bad credit, that'll affect your mortgage eligibility. Speak to the lender about whether you can qualify for the mortgage using only your credit score.

Does Having Multiple Credit Cards Help Or Hurt Your Path To An 800 Credit Score?

Having multiple credit cards can actually help you reach an 800 credit score, as long as you manage them responsibly. People with perfect 850 scores have an average of 5.8 credit cards. The key is to keep your total credit utilization low across all cards and never miss payments on any of them. More cards mean more available credit, which can lower your overall utilization ratio.